Dec 10 - Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

AAII MEMBERS CROWD THE NEUTRAL CAMP (1249 EST/1749 GMT)

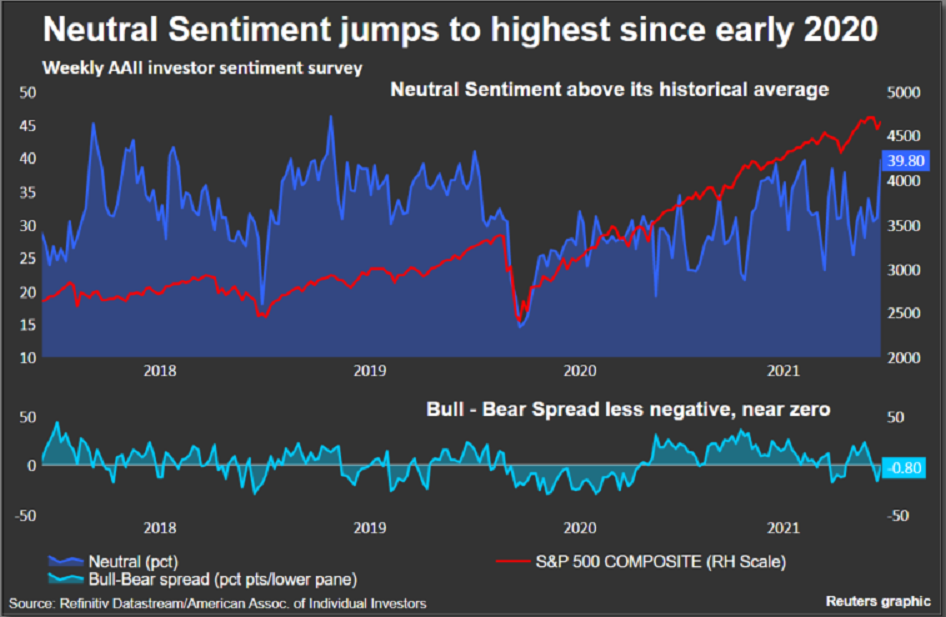

The percentage of investors with a "neutral" short-term outlook for the U.S. stock market is at its highest level in nearly two years in the latest American Association of Individual Investors Sentiment Survey (AAII). With this, bearish sentiment posted a significant decline.

Register now for FREE unlimited access to reuters.com

AAII reported that neutral sentiment, or expectations that stock prices will stay essentially unchanged over the next six months, rose by 8.8 percentage points to 39.8%. Neutral sentiment was last higher in early January 2020 (40.9%). The historical average is 31.5%.

Bullish sentiment, or expectations that stock prices will rise over the next six months, gained by 3.1 percentage points to 29.7%. This is the third consecutive week that bullish sentiment remains below the historical average of 38.0%.

Bearish sentiment, or expectations that stock prices will fall over the next six months, collapsed by 11.9 percentage points to 30.5%. This week’s reading matches the historical average. The significant decline in bearish sentiment follows last week’s reading of 42.4%, which was the highest level since Aug. 19, 2020.

With these changes, the bull-bear spread increased to -0.8 from -15.7 last week read more :

(Terence Gabriel)

*****

EUROPEAN STOCKS NOTCH BEST WEEK IN 9 MONTHS (1200 EST/1700 GMT)

European shares slipped but still managed to close with their best week since March thanks to a strong rebound earlier this week on signs that the Omicron variant could be less harmful than initially feared.

Some strategists also suggested that there was a bit of buy-the-dip move too after November's sharp sell off.

"Animal spirits kicked in, this week pushing markets up again, almost retracing the entire recent drawdown," says Emmanuel Cau, European equity strategist at Barclays.

The pan European STOXX 600 index (.STOXX) was down 0.3% for the day but rose 2.8% for the week, its best week nine months.

The recent easing in the rally, with the STOXX declining for three consecutive days, is a reflection of the realisation that even if Omicron isn't as severe as initially feared, "concern is still elevated that this good news on severity could be outweighed by a rise in transmissibility", Deutsche Bank's Jim Reid says.

(Joice Alves)

*****

GREEN CHRISTMAS: PRICES REMAIN HOT, BUT SO DO WAGES (1110 EST/1610 GMT)

A stubbornly hobbled supply chain and an increasingly tight labor market have launched prices into orbit, a state of affairs about which the U.S. consumer, who does the economic heavy lifting, doesn't seem overly concerned about, with Santa on his way.

Consumer prices (USCPI=ECI) jumped by 0.8% in November, marking a slight deceleration from the prior month's 0.9% gain and coming in 0.1 percentage points higher than expected.

Line-by-line, the Labor Department's consumer price index (CPI), which measures the prices urban U.S. consumers pay for a basket of items, showed gasoline, air fares and autos saw some of the hottest growth, with a 3.5% jump in energy prices lifting the headline number.

Year-over-year, CPI jumped 6.8% (USCPNY=ECI), the highest reading in 39 years. And it's not over yet.

"Ongoing supply disruptions will continue to place upward pressure on consumer prices," writes Kathy Bostjancic, chief U.S. economist at Oxford Economics.

The closely-watched 'core' CPI (USCPFY=ECI), which strips out volatile food and energy prices, accelerated by 0.3 percentage points to a 4.9% annual growth rate, inline with expectations.

Taken together with economic data released earlier this week, which showed the quit rate hitting a record and job openings hovering at 11 million, all signs are pointing toward price spikes long overstaying their welcome and suggest the U.S. Federal Reserve could very well start tightening its accommodative monetary policy sooner than many might have hoped.

"It’s not going to cause jitters in the market because elevated inflation is already priced into the market," says Peter Cardillo, chief market economist at Spartan Capital Securities in New York. " But this does mean we’re probably going to be faced by a more hawkish Fed and a change in monetary policy is likely to happen in the latter part of the second quarter of 2022."

Here's a look at the core CPI trendline, which continues to soar well above the Fed's average annual 2% target:

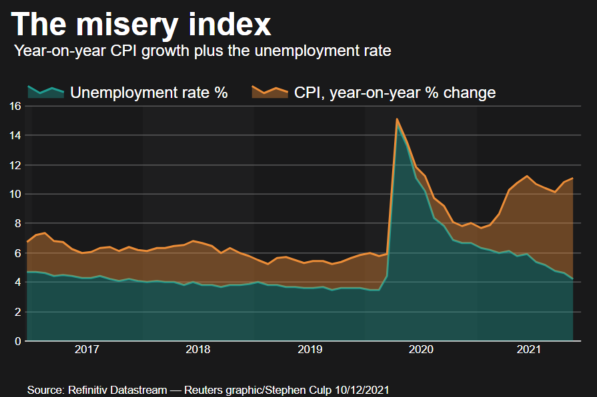

Now would be an excellent time to revisit our old crotchety friend the misery index.

The misery index takes various forms, but for our purposes it's the unemployment rate plus annual headline CPI growth.

Even with the jobless rate having edged down to 4.2%, elevated consumer prices are holding the misery index well above pre-pandemic levels:

So what do consumers make of this lump of inflationary coal in their stocking as the holiday season approaches?

With wages rising along with consumer prices, they don't seem overly concerned.

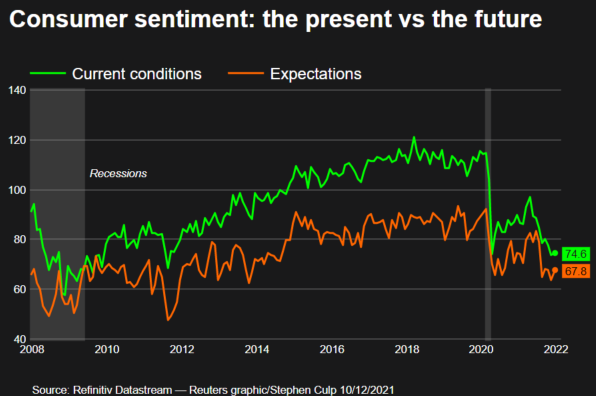

The University of Michigan's preliminary take on current month Consumer Sentiment (USUMSP=ECI) showed the consumer's mood brightening.

The index's December reading unexpectedly gained 3 points to a print of 70.4, moving in the opposite direction than economists predicted.

Both 'current conditions' and 'expectations' components gained ground, with one- and five-year inflation expectations holding firm at 4.9% and 3%, respectively.

But what Richard Curtin, chief economist at UMich's Surveys of Consumers, finds most interesting, was the substantially brightened mood among the survey's lowest-earning respondents.

"While small differences in the direction of change are rather common, it is quite unusual to record such a large change in the bottom third: a larger one-month percentage was recorded only once before, a gain of 29.2% in June 1980," Curtin writes.

The reason for this? Rising wages.

"The core of the renewed optimism among the bottom third was the expectation of income increases of 2.9% during the year ahead; the last time a higher gain for this group was expected was in 1981," Curtin adds. "This suggests an emerging wage-price spiral that could propel inflation higher in the years ahead."

As the graphic below shows, however, consumer attitudes regarding the current state of affairs and what they see in their immediate future remain well below pre-pandemic levels:

While the CPI report came in hot, the markets expected it to do just that. And Wall Street, allergic to surprises, gained ground in early trade.

However, the enthusiasm has waned. The major indexes are now mixed, with the Dow (.DJI) and Nasdaq (.IXIC) slightly red. The S&P 500 (.SPX) is clinging to a slight gain.

(Stephen Culp)

*****

U.S. STOCKS STRUGGLE TO HOLD GAINS IN EARLY TRADE (1001 EST/1501 GMT)

Wall Street's main indexes are rallying on Friday after data showed consumer prices rose largely in line with estimates last month, taking some pressure off investors concerned about aggressive tightening of monetary policy.

That said, initial pops have quickly deflated with the indexes now posting just modest gains.

The U.S. 10-Year Treasury yield is falling back to the 1.47% area, and growth (.IGX) is slightly outpacing value (.IVX).

Chips (.SOX) and tech (.SPLRCT) are among outperformers, while banks (.SPXBK) are among the losers.

Even though crude and natural gas futures are both gaining, energy (.SPNY) is red in early trade.

Here is where markets stand:

(Terence Gabriel)

*****

IS THE DRAGON RUNNING OUT OF FIRE? (0919 EST/1419 GMT)

The Nasdaq Golden Dragon China index (.HXC) which tracks the performance of U.S.-listed China stocks is down 38.6% this year, on course for its worst yearly performance since 2008. This is not the year of the dragon.

The index fell 9.1% on Dec. 3, its worst performance in over 13 years, after Didi Global Inc (DIDI.N) said it planned to delist from the NYSE, with the ride hailing giant dropping 22.1% and bringing down other Chinese ADRs with it. read more

Things went south pretty quickly after the index hit a record high in February 2021, losing half its value as regulatory pressures from Beijing and Washington weighed.

Frank Benzimra, head of Asia equity strategy at Societe Generale, finds that in Chinese equity, Common Prosperity stocks, from Green Tech to New Infrastructure outperformed this year.

"Being on the right of China authorities’ policy agenda mattered more than valuations," Benzimra said in a note.

The good news for Didi, that is now planning a Hong Kong listing, is that HK-listed shares have outperformed their U.S.counterparts. Although when it comes to Chinese equity, onshore stocks have been relatively resilient to both, according to Benzimra's note.

On the retail end, analysts at Vanda Research found that retail purchases of China ADRs were negligible after Didi's de-listing.

"After multiple attempts to buy-the-dip, we suspect retail investors have gotten tired of trying to catch a falling knife," wrote Giacomo Pierantoni and Ben Onatibia, in a note.

(Bansari Mayur Kamdar)

*****

DOW INDUSTRIALS POISED TO POP POST CPI (0900 EST/1400 GMT)

In the wake of mostly in-line November CPI data , CBT e-mini Dow Futures are posting premarket gains suggesting the Dow Jones Industrial Average (.DJI) is poised to rise around 200 points when regular-session trading kicks off on Friday:

In that event, the DJI can challenge the 76.4%/78.6% Fibonacci retracement zone of its November-December slide at 35,961.87/36,018.16. Traders will be watching for how the Dow deals with this barrier.

The next levels above this zone include the November 16 high at 36,316.61, the November 8 record close at 36,432.22 and the November 8 record intraday high at 36,565.73. The resistance line from early 2018, which capped strength in November, is now close to 37,000.

A failure to overwhelm the retracement zone, followed by a reversal below Thursday's low at 35,577.14, however, can add credence to the view that December strength has just been a counter-trend bounce. read more

(Terence Gabriel)

*****

FOR FRIDAY'S LIVE MARKETS' POSTS PRIOR TO 0900 EST/1400 GMT - CLICK HERE: read more

Register now for FREE unlimited access to reuters.com

Terence Gabriel is a Reuters market analyst. The views expressed are his own

Our Standards: The Thomson Reuters Trust Principles.

"crowd" - Google News

December 11, 2021 at 01:02AM

https://ift.tt/3IEQCfD

LIVE MARKETS AAII members crowd the neutral camp - Reuters

"crowd" - Google News

https://ift.tt/2YpUyMI

https://ift.tt/2KQD83I

Bagikan Berita Ini

0 Response to "LIVE MARKETS AAII members crowd the neutral camp - Reuters"

Post a Comment